Solo 401k vs. SEP IRA: Which Plan Grows Your Wealth Faster?

Solo 401k vs. SEP IRA: The Secret to Maximizing Your Retirement Savings

Are you a self-employed professional, freelancer, or small business owner? Then you already know that saving for retirement is all on you. No pension, no automatic employer match—just you and the choices you make today.

So let’s get real. You need a plan that lets you put away the most money, save on taxes, and build wealth faster than the average investor. But there are two heavyweight contenders battling for your attention: the Solo 401k and the SEP IRA.

Which one will make you the most money? Which one will give you the biggest tax advantages? And which one will put you in control of your future?

The answer lies ahead.

What’s a Solo 401k? And Why Is It So Powerful?

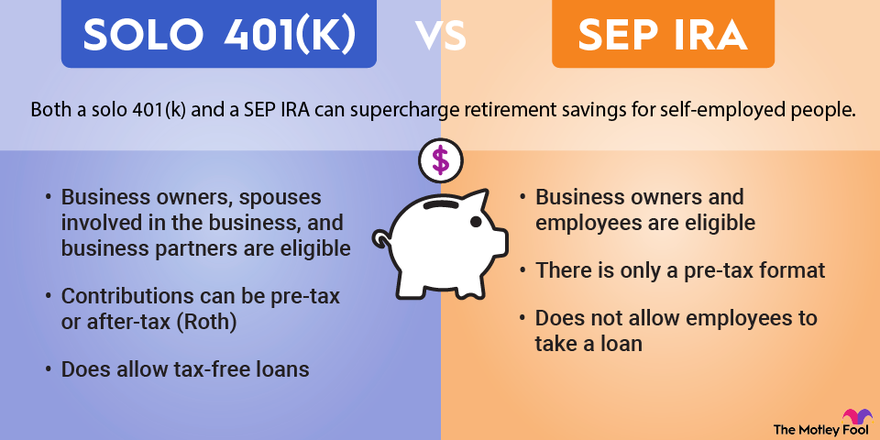

Imagine a retirement account that lets you contribute as both the employee and the employer. That’s exactly what a Solo 401k does. Unlike traditional 401ks, which require a company full of employees, the Solo 401k is built just for you—the independent business owner, consultant, or freelancer.

Here’s Why High Earners Love the Solo 401k:

✔ Massive Contribution Limits – Up to $69,000 per year (or $76,500 if you’re 50+). That’s double what most SEP IRAs allow at lower income levels.

✔ Roth or Pre-Tax? Your Choice. – Want tax-free withdrawals later? Go Roth. Want to reduce your taxable income today? Choose pre-tax. You decide.

✔ Take a Loan Against Your Savings. – Need access to cash? Borrow up to $50,000 from your own plan. SEP IRAs don’t let you do this.

✔ Invest in Anything. – Stocks, bonds, real estate, crypto—you call the shots. Many retirement plans limit your choices. The Solo 401k puts you in control.

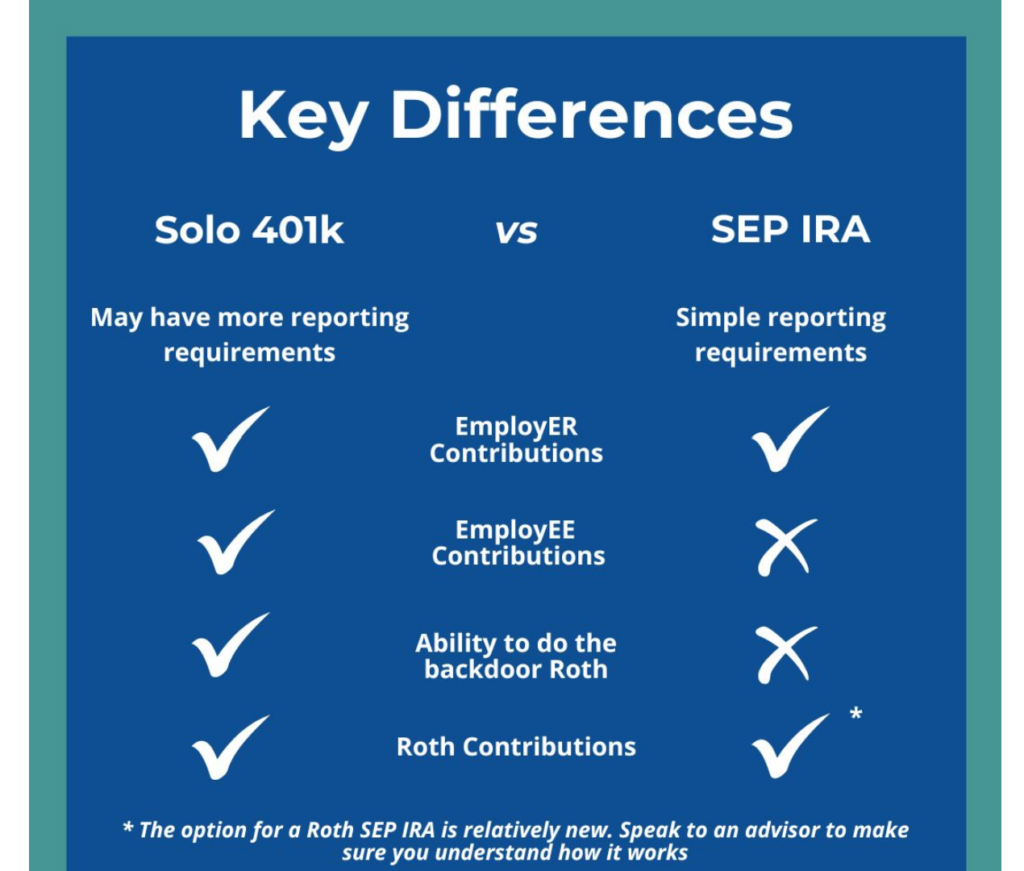

What About the SEP IRA? Simpler, But Is It Enough?

Now, let’s talk about the SEP IRA—the traditional go-to for self-employed individuals. It’s easy to set up, doesn’t require much paperwork, and offers solid tax-deferred growth.

Here’s Why Business Owners Choose the SEP IRA:

✔ Super Simple Setup – No complex forms. No annual IRS filings. Just sign up and start contributing.

✔ High Contribution Limits—If Your Income Is High Enough – You can contribute 25% of your net earnings, up to $69,000 per year.

✔ Great for Businesses with Employees – Unlike a Solo 401k, a SEP IRA works even if you have staff. But there’s a catch: you must contribute the same percentage for every employee as you do for yourself.

✔ Tax Savings Today – Like the Solo 401k, SEP IRAs let you defer taxes until retirement. But you don’t get a Roth option—so no tax-free withdrawals later.

Solo 401k vs. SEP IRA: The Brutal Truth

1️⃣ Who Can Contribute More?

- Solo 401k: Up to $69,000 ($76,500 if 50+), even at lower income levels.

- SEP IRA: Limited to 25% of your net self-employment income—so lower earners can’t contribute as much.

2️⃣ Who Gets More Tax Flexibility?

- Solo 401k: Offers both Roth and pre-tax options.

- SEP IRA: Only pre-tax contributions allowed—meaning you pay taxes on everything later.

3️⃣ Who Can Borrow From Their Plan?

- Solo 401k: Yes—loans up to $50,000 available.

- SEP IRA: No loan option at all.

4️⃣ Who Has Less Paperwork?

- Solo 401k: Requires a little more admin work, especially once the account grows past $250,000.

- SEP IRA: Almost no paperwork—a big plus for some business owners.

The Million-Dollar Question: Which One Should You Pick?

Go with a Solo 401k if:

✅ You want the highest contribution limits, even with moderate income.

✅ You like the idea of Roth contributions and tax-free withdrawals later.

✅ You might want to take a loan against your retirement savings.

✅ You’re a self-employed individual with no employees (except a spouse).

✅ You want the widest range of investment options.

📷 Image Idea: A graphic showing a freelancer maxing out a Solo 401k.

Go with a SEP IRA if:

✅ You want something simple with minimal paperwork.

✅ You’re okay with pre-tax savings only (no Roth option).

✅ You own a business with employees and need to offer them retirement benefits.

✅ You prefer an easy setup with fewer reporting requirements.

📷 Image Idea: A business owner comparing a Solo 401k and SEP IRA at a desk.

Final Verdict: Which One Builds Wealth Faster?

Both plans have their strengths. But if you’re looking to put away the most money, get the most flexibility, and build wealth faster, the Solo 401k wins hands down.

However, the SEP IRA is still a great choice if you need a simple plan with less paperwork—especially if you have employees.

Next Steps: Don’t Just Think About It—Take Action!

✔ Talk to your financial advisor – See which plan fits your long-term goals.

✔ Check with your 401k provider or brokerage – Find out what Solo 401k and SEP IRA options are available to you.

✔ Start contributing today – The earlier you start, the more you can grow tax-free.

✔ Download Our Free Guide – Want to make sure you’re not making any 401k mistakes? Get our free PDF: “10 Mistakes That Can Ruin Your 401k – And How to Avoid Them.”

🚨 Free 30-Day Plan to Grow Your 401(k) Faster—Get Yours Now!

[Enter Your Email Below]