401k After Tax Contributions The Secret to Tax Free Millions

401(k) After-Tax Contributions: The Game-Changing Strategy You Never Knew You Needed

Imagine pouring every spare dollar into your 401k plan, hoping for a comfortable retirement. But deep down, you wonder: Am I truly making the most of my savings? That fear—the thought of leaving money on the table—drives many to look for better strategies.

One of the best-kept secrets in retirement planning is 401k after-tax contributions. Most people know about traditional and Roth 401ks. But few realize there’s another level—a way to stash even more money, convert it into tax-free growth, and build a larger nest egg. The question is: Are you ready to take advantage of it?

Why 401k After-Tax Contributions Matter

Many people suspect they could be doing more for retirement. They max out their pre-tax contributions and wonder, What’s next? The answer might be after-tax 401k contributions.

The Missing Piece

Saving the usual pre-tax amount is a good start. However, those who aim for a secure retirement need more than discipline—they need a strategy. After-tax 401k contributions provide an opportunity to save beyond traditional limits and reduce future tax burdens.

What Are After-Tax 401k Contributions?

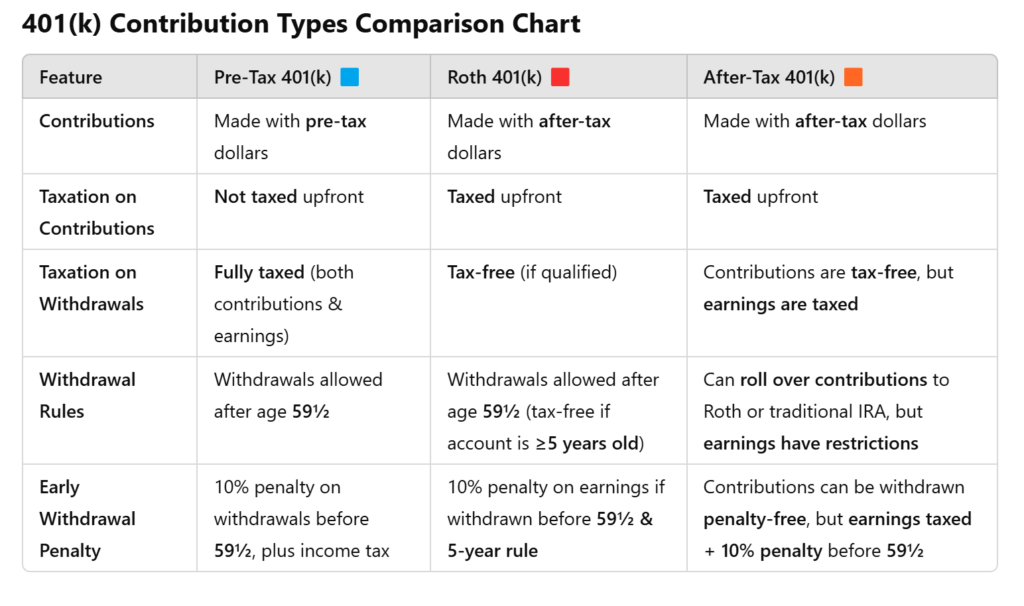

Most people understand pre-tax contributions: You put money into your 401k before taxes, lowering taxable income now but paying taxes on withdrawals later. Roth 401ks work the opposite way—you pay taxes upfront but withdraw tax-free in retirement.

After-tax 401k contributions work differently:

- After-Tax Input: Contributions come from income that has already been taxed.

- Tax-Deferred Growth: Earnings grow without annual taxation.

- Withdrawal Rules: Contributions aren’t taxed again, but earnings are—unless converted into a Roth.

The real magic happens when these contributions move into a Roth IRA or Roth 401k, ensuring tax-free growth forever.

.

.

Who Benefits Most from After-Tax 401k Contributions?

Not everyone needs this strategy. But if you fit these criteria, it could change your financial future:

- You’ve Maxed Out Your 401k – In 2024, the limit is $23,000 (or $30,500 if you’re 50+). If you want to save more, this option lets you go beyond the cap.

- Your Employer Allows a Mega Backdoor Roth – Some plans allow rolling after-tax contributions into a Roth IRA or Roth 401k. If yours does, you could unlock serious tax-free growth.

- You Want to Reduce Future Taxes – By converting after-tax contributions into a Roth, you shield future gains from taxation.

- You’re a High Earner – If you’ve maxed out traditional retirement savings and want to stash more, this could be your best move.

How the Mega Backdoor Roth Works

The Process

Let’s break it down:

- You contribute after-tax money beyond the normal 401k limit.

- Your employer allows in-service rollovers or Roth conversions.

- You move funds into a Roth IRA or Roth 401k.

- Your money grows tax-free from that point forward.

📷 Image Idea: A side-by-side chart comparing standard 401k savings vs. Mega Backdoor Roth conversions.

Why This Strategy Works

- Timing is key – The faster you convert, the fewer earnings are taxed.

- Your Roth balance grows – More tax-free money means a better retirement.

- It maximizes IRS limits – The 401k limit includes employer contributions. With this strategy, you get closer to the $69,000 total limit ($76,500 for 50+ savers).

A Real-World Example

Sarah, 45, contributes the $23,000 max pre-tax. Her employer adds $10,000 in matching funds. That leaves $36,000 of space in her 401k. She puts that amount into after-tax contributions. Her plan allows immediate Roth conversions, so she moves it all into a Roth IRA.

After 20 years at a 7% return, that single year’s conversion grows to over $145,000 tax-free. If she does this every year, she could add millions to her retirement—without worrying about future tax hikes.

Watch Out for These Pitfalls

No strategy is perfect. Here’s what to consider before diving in:

❌ Not All Employers Allow It – Some 401k plans don’t permit after-tax contributions or in-service rollovers.

❌ Pro-Rata Taxation Rules – If you don’t convert quickly, earnings could be taxed.

❌ Paperwork & Complexity – This isn’t a “set it and forget it” approach. Tracking contributions and conversions requires diligence. ❌ Not Always the Best Option – If your plan has high fees or poor investment options, a Roth IRA or taxable brokerage account might be better.

The Final Takeaway: Is This Strategy Right for You?

If you’re maxing out your 401k and your employer supports after-tax contributions, this strategy could supercharge your retirement savings. However, it requires active management to maximize its benefits.

Steps to Take Right Now

✅ Check your plan’s rules – See if after-tax contributions and in-service rollovers are allowed.

✅ Talk to a financial advisor – A tax professional can help navigate rollovers.

✅ Automate your contributions – If your plan allows it, set up automatic after-tax contributions and conversions.

✅ Download Our Free Guide – Want to avoid costly mistakes? Get our free PDF: “10 Mistakes That Can Ruin Your 401k – And How to Avoid Them.”

📥 Download Your Free Guide Now