What is a 401(k) Plan A Simple Guide

What is a 401(k) Plan? A Simple Guide for Young Professionals

Why You Need to Know About 401(k) Plans

If you’re a young professional just starting your career, planning for retirement might be the last thing on your mind. After all, there are more immediate financial concerns—rent, student loans, and maybe even saving up for a dream vacation. But here’s the truth: the earlier you start saving for retirement, the easier it will be to build long-term wealth. And one of the best tools available for that? Your 401(k) plan.

What is a 401(k) Plan?

A 401(k) plan is a retirement savings account offered by many employers that allows you to contribute a portion of your salary before taxes. Some employers even match a percentage of your contributions—essentially giving you free money for your retirement savings.

How Does a 401(k) Work?

- You Contribute Money Automatically: A portion of your paycheck is deducted and deposited into your 401(k) before taxes.

- Your Employer Might Match Contributions: Some employers match a percentage of what you contribute.

- Your Money is Invested: Funds are placed into stocks, bonds, or mutual funds.

- Taxes Are Deferred Until You Withdraw: Traditional 401(k)s allow for tax-deferred growth

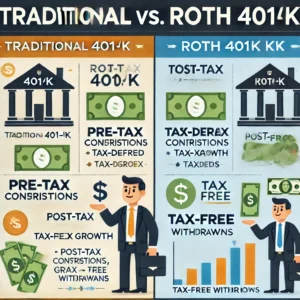

Roth vs. Traditional 401(k): Which One is Right for You?

Choosing between a Traditional and Roth 401(k) depends on when you want to pay taxes.

Traditional 401(k): Contributions are tax-deductible now, but taxed upon withdrawal.

Roth 401(k): Contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

How Much Should You Contribute?

The general rule of thumb is to contribute at least enough to get the full employer match—otherwise, you’re leaving free money on the table.

What About Freelancers and the Self-Employed? Enter the Solo 401(k)

If you’re self-employed or a freelancer, a Solo 401(k) allows you to contribute both as an employee and employer, maximizing savings.

Common 401(k) Mistakes to Avoid

- Not contributing enough to get the employer match.

- Ignoring fees that can reduce investment growth.

- Withdrawing money early and facing penalties.

- Not increasing contributions over time.

The Power of Compound Interest Over Time

Starting your 401(k) now is one of the smartest financial moves you can make. Even small contributions today can grow into a substantial retirement fund thanks to the power of compound interest.

Ready to Take Action?

Don’t just read about it—take action! Sign up for our 30-Day 401(k) Action Plan to get a step-by-step guide on optimizing your retirement savings.